Direct Indexing: The Past, Present, and Future of Personalized Investing

Once reserved for institutions and ultra-high-net-worth families, direct indexing has quietly evolved into one of the most innovative investment tools in decades.

It’s a strategy that lets investors build a portfolio mirroring an index (think S&P 500 or the EAFE) but with customization, tax optimization, and control that mutual funds and ETFs can’t match.

It’s an investment vehicle I’ve followed for years and one that BlackRock promoted at their recent Advisor Forum Conference, which I attended this week.

The History

Direct indexing first gained traction in the 1990s and early 2000s, primarily used for tax-loss harvesting in taxable accounts.

Firms like Aperio and Parametric pioneered the approach, offering separately managed accounts (SMAs) that replicated the holdings of major indices.

Back then, you needed millions to invest and had to deal with higher costs and friction just to get started.

In other words, direct indexing wasn’t “direct” for most; it was exclusive.

Two developments changed the game:

Zero-Commission Trading

Once brokerages removed fees on stock trades, the cost barrier dropped dramatically.

Technology Enhancements

Lower transaction costs and better portfolio management software made it possible to efficiently manage hundreds of individual stocks at scale.

These shifts opened the door for direct indexing to reach a broader investor base.

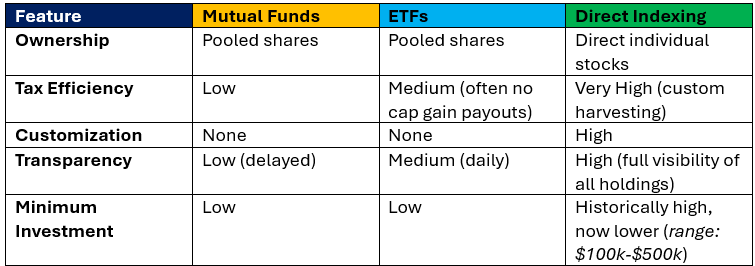

Direct Indexing vs. Mutual Funds vs. ETFs

Direct indexing involves owning the underlying securities of an index directly instead of buying a fund that tracks the index.

That means instead of holding a single ETF, you own each stock.

I like to compare it to a smoothie and its ingredients.

A smoothie is a like mutual fund or ETF. You “blend” in all the companies together to get a beautifully diversified fund.

With direct indexing you hold the individual “ingredients”.

If you don’t like raspberries, throw them out – banana’s rotten (i.e., stock is at a loss), get rid of it.

Here’s a fun diagram comparing the three vehicles:

The Benefits

Direct indexing allows investors to get the same market exposure as funds and ETFs, plus one big advantage: the ability to offset capital gains through tax loss harvesting.

The Basics: Tax-loss harvesting is the process of selling positions that are down, “harvest” (i.e., recognize) the loss. These losses can offset capital gains elsewhere in your portfolio, reducing your tax bill.

While ETFs and mutual funds also own the underlying securities, they don’t allow you to harvest individual losses unless you sell the entire fund.

If your ETF is up, there’s no reason to sell it, so there are no losses to harvest.

But with direct indexing, loss can occur even in a rising market.

For example, the S&P 500 was up 23% in 2024 (see chart below):

However, according to JP Morgan’s Guide to the Market, nearly 150 companies in the index were down 5% or more.

In any given year, almost 30% of stocks finish the year negative, and about 75% of stocks drop at least 5% at some point.

There’s a lot of opportunity to tax loss harvest even in up years.

Most direct indexing strategies harvest losses throughout the year, not just in December.

Even if you haven’t realized any capital gains in a calendar year, you can still use up to $3,000 in realized losses to reduce your ordinary income.

Any excess losses can be carried forward to future years.

Over time, these small tax breaks can quietly compound into real savings, especially as your portfolio grows.

Here are a few more benefits to consider:

Reduce Concentrated Positions

You can contribute appreciated stock alongside cash, and the strategy can pair gains with harvested losses.

If you have a concentrated position outside the strategy, direct indexing can avoid that sector entirely to reduce exposure.

Maximize Charitable Giving

Since you own individual stocks, you can donate your most appreciated shares to charity, boosting both your philanthropic impact and your tax benefits.

Customization

You can avoid companies that don’t align with your values or investment principles.

Capital Gain Harvesting

This is the opposite of tax loss harvesting.

People in the 10%-12% tax brackets could realize between $48k-$96k (depending on filing status) in capital gains with 0% tax consequences.

The Downside

Direct indexing isn’t perfect for everyone.

There are still minimum investment requirements, and the tax benefits only apply to taxable accounts.

Also, the more customized your portfolio (e.g., by eliminating certain sectors or companies), the higher your tracking error or the difference between your portfolio’s returns and the benchmark index.

One more important note: from what I’ve seen and heard from managers, the tax-loss harvesting benefits tend to taper off after 6–10 years, depending on market conditions.

That makes sense because the market goes up over time, and eventually, you run out of losers to sell.

At that point, you’re essentially left with a more expensive version of an index fund.

There are a couple of ways to continue the benefits of tax loss harvesting:

Continue adding cash to the strategy

Consider overlay strategies like shorting securities (though this adds complexity, cost, and risk)

Final Thoughts

As investors demand more personalization and tax efficiency, direct indexing offers a compelling solution.

It’s no longer just about tracking an index; it’s about owning it on your own terms.

Keep learning. Keep growing. Keep going.

Now here’s what I’ve been reading, listening, and watching:

Arnold Schwarzenegger (The man who focused on what mattered) on Founders

Just Keep Buying by Nick Maggiulli

The Seven Frequencies of Communication by Erwin Raphael McManus

The 5 Types of Wealth by Sahil Bloom

Children’s book (I have a 5-year old): Rock and Moss: The Physics of Friendship by Lindsay Leslie

Here’s what I’ve been writing: