Value Is Winning Again

Value is back, baby.

For most of the last two decades, growth stocks have dominated investors’ attention. Companies that have reinvested heavily in future growth (often at high valuations) have outperformed their value-oriented peers.

The Basics: Value stocks tend to be established companies trading at lower prices relative to their earnings or assets, while growth stocks are priced higher today because investors expect faster future growth.

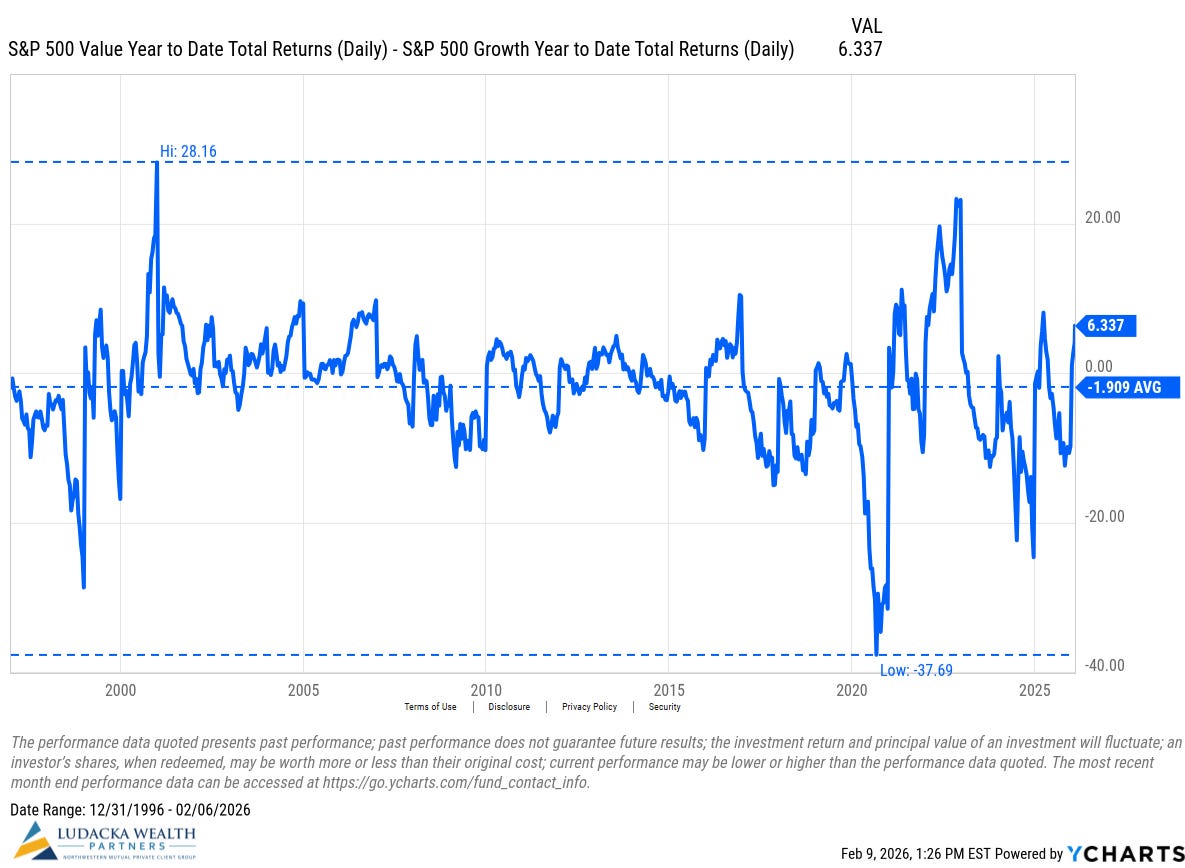

Over the last 25 years, value has lagged growth by roughly 2% per year on average, given the extreme returns growth has delivered in the last five years (see chart below):

But nothing remains permanent in the stock market.

So far this year, the S&P 500 Value Index has outperformed the S&P 500 Growth Index by about 6%, well above its long-term average (see chart below):

There has always been this tug-of-war of performance between the two investing styles.

During the late 1990s dot-com boom, growth was the only place investors wanted to be, until the bubble popped. In the early 2000s, value dramatically outperformed growth, beating it by about 28% annually at its peak.

Fast-forward to the post-COVID years. Stimulus checks, zero interest rates, and speculation fueled another growth surge. At one point, growth stocks outperformed value by more than 38%.

Then, interest rates rose quickly, along with the cost of capital, which decimated many fast-growing companies.

One reason value has regained momentum this year comes down to sector exposure.

Energy and Consumer Staples (two of the best-performing sectors year-to-date) make up about 16% of the S&P 500 Value Index. In the S&P 500 Growth Index, those same sectors represent just 1%.

On the flip side, the Technology sector makes up about 47% of the Growth Index. When tech is leading, growth looks brilliant. But so far this year, technology has been the worst-performing sector, down about 3%.

Does this mean growth is over? Of course not.

Value and growth take turns leading, often for reasons that only make sense in hindsight. Trying to time those rotations usually leads investors to chase what just worked and abandon what didn’t, often at exactly the wrong moment.

The takeaway is to stay diversified across styles.

A portfolio that balances value and growth isn’t exciting in any single year. But over time, it helps investors participate when leadership shifts.

And right now, value is having its moment again.

Keep learning. Keep growing. Keep going.

Now here’s what I’ve been reading, listening, and watching:

Marc Andreessen: The real AI boom hasn’t even started yet by a16z

Listened to the following earnings calls: Merck, AMD, Alphabet, Chubb, The Cigna Group, Blue Owl Capital, Illumina, Amazon, Philip Morris International plus Cisco’s AI Summit

The Valuation Treadmill by James Park

Children’s Books (I have a 6-year old and a newborn): What If You Had Animal Teeth? by Sandra Markle (Author), Howard McWilliam (Illustrator)

Here’s what I’ve been writing: