Halfway There: Reviewing the Stock Market’s First Half of 2025

Whoa, we're halfway there

Oh, livin' on a prayer

- Bon Jovi (1986)

That song is going to get stuck in your head now. You’re welcome.

The first six months of 2025 are officially in the books.

While headlines have been all over the place (e.g., tariffs, trade deals, and AI booms), the major U.S. stock indexes have delivered respectable gains.

Here’s a recap of the year so far.

U.S. Performance

Through the first half of the year:

The S&P 500 (a proxy for U.S. large stocks) rose 5.5% year-to-date, hitting a fresh all-time high the final week of June.

The Dow Jones Industrial Average (a proxy for 30 large, well-known U.S. companies) is up roughly 4% for the year.

The NASDAQ Composite (a proxy for technology and growth stocks) also hit record territory, climbing 5.5% since January.

Despite a rocky spring (who can forget the sharp drop in April?), U.S. stocks have roared back, and the bull market that began in October 2022 is still alive.

What has helped U.S. stocks regain their footing? Less uncertainty.

The last two and a half months have delivered a few surprises that turned early-year caution into cautious optimism.

On April 2 (famously known as “Liberation Day”), President Trump announced sweeping new tariffs that rattled the market.

Stock and bond markets reacted immediately and viscerally.

The current administration quickly pivoted and postponed the announced tariffs.

As Trump put it, the market was “a little yippy and afraid.”

Fewer tariffs meant better prospects for corporate earnings, less chance of a recession, and more clarity for business owners and consumers.

With U.S. and China trade talks moving forward, uncertainty continues to ease.

Another reason stocks kept climbing is that Big Tech refuses to tap the brakes on AI (artificial intelligence) spending.

Earlier this year, there was chatter that the tech giants would pull back after DeepSeek was released in January.

But these tech giants have made it clear: the AI arms race is still on.

What’s Going On with the Magnificent Seven?

The Magnificent Seven (i.e., Apple, Alphabet, Amazon, Microsoft, Meta, Nvidia, and Tesla) have slowed their all-powerful ascent this year, at least a few of them have.

A summary of the results:

The S&P 500 (dark blue line), as mentioned, is up 5%.

The S&P 493 (light blue line, which excludes the Magnificent Seven) is doing better: up 7.0%.

The Magnificent Seven is trailing the pack: up 2% year-to-date.

That’s unusual.

For years, these behemoths have dominated index returns, partly because they generate massive earnings growth and partly because investors have been willing to pay eye-watering valuations for them.

But this year, the group is showing some cracks.

One outlier is Nvidia, which surpassed Apple and Microsoft to become the world’s largest company (again), thanks to relentless AI demand.

Nvidia now sits at a $3.8 trillion market cap, with Microsoft slightly behind at $3.7 trillion.

Not every Mag 7 titan is winning.

So far in 2025, four of the seven (Apple, Amazon, Alphabet, and Tesla) are underperforming the S&P 500.

It’s hard to stay at the top.

Apple has been a big drag, down nearly 18% year-to-date.

Much of this stems from its sluggish AI rollout. Rumors swirl about a potential acquisition to catch up, but investors are losing patience.

Tesla is wrestling with a different narrative.

Elon Musk’s political commentary hasn’t helped global sales. However, die-hard fans were encouraged by the rollout of robotaxis in Texas and Musk’s promise to spend more time focusing on his companies.

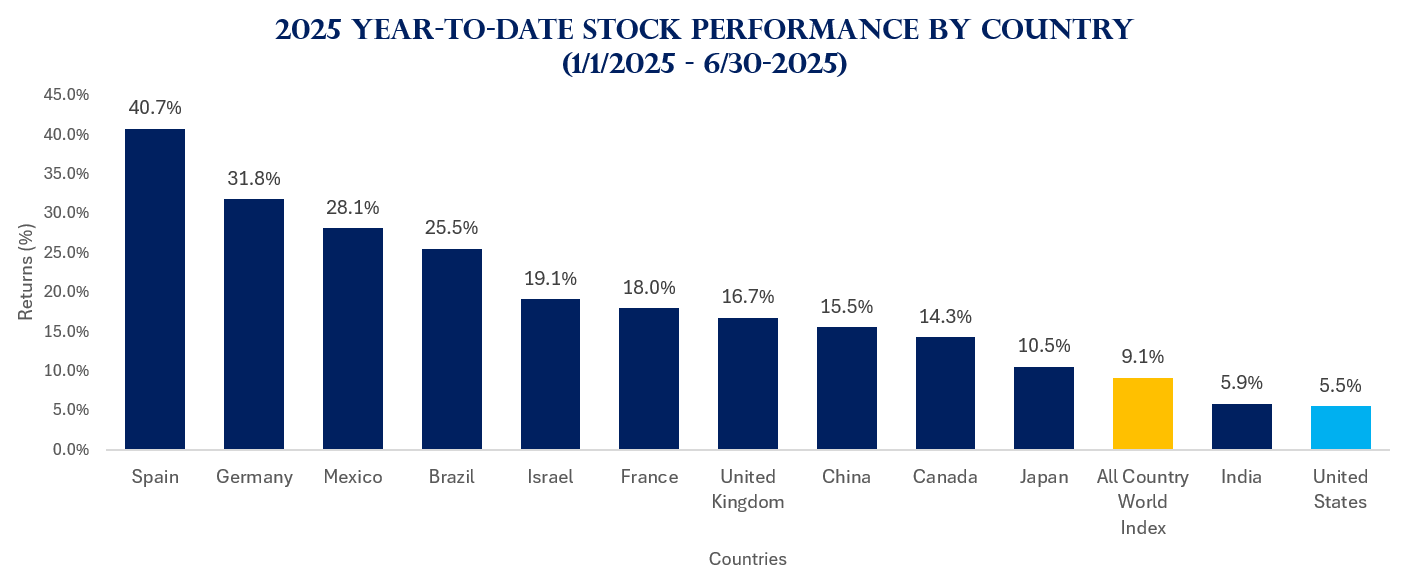

Performance Around the World

Here’s something that might surprise American investors who are used to seeing the U.S. on top: in 2025, it’s near the bottom of the global leaderboard.

Spain, Germany, France, Brazil, Mexico, Canada, the UK, Israel, Japan, and India are all outperforming the U.S. this year.

The All-Country World Index (ACWI), which includes 23 developed and 24 emerging stock markets, is ahead, too.

Here we can see how different asset classes have performed through the first half of 2025:

Small-cap stocks are negative for the year and face real headwinds.

Compared to large stocks, small stocks carry a lot more variable-rate debt (see the chart from Apollo below):

Rising rates over the last two years have made that debt more expensive, which has hurt growth.

Risks on the Radar

Risk is what’s left over when you think you’ve thought of everything. – Carl Richards

Risks are always present in the markets. Here are just a few:

July 9 looms large, as that is the date when Trump’s big tariff package could snap back if trade negotiations stall. If they do, the markets won’t like it.

Consumers and business owners remain concerned (although less so than April’s peak).

U.S. large-cap market-cap-weighted valuations remain stretched.

Valuations is not a great short-term timing tool, but over the long run, they matter.

Final Thoughts

The first half of 2025 reminds us there’s always something to worry about, but sitting on the sidelines rarely works.

The market has rewarded those who can stomach the uncertainty.

The bull market is still intact.

And while risks remain, so do reasons for optimism.

Onward to the second half.

Keep learning. Keep growing. Keep going.

Now here’s what I’ve been reading, listening, and watching:

Ernest Shackleton (the man who kept his 27 man crew alive for nearly two years in Antarctica) on Founders

Just Keep Buying by Nick Maggiulli

The Seven Frequencies of Communication by Erwin Raphael McManus

The 5 Types of Wealth by Sahil Bloom

Children’s book (I have a 5-year old): If I Were President by Catherine Stier

Here’s what I’ve been writing: